Global trade in goods and services exceeds $35 trillion dollars a year, and moves billions of tons of primary materials, commodities, and finished goods annually. The supply chains that produce, process, ship, store, and retail that material output account for 60% of global carbon emissions. And while there are many supply chains, eight of them alone are half of global emissions, and just one, food, is a quarter of all annual greenhouse gases. Modern economies do not exist without supply chains; those supply chains, in turn, do not exist today without structural emissions and planet-scale strain on the climate system.

In this letter, Voyager outlines the state of supply chains today, how climate change and its responses are changing the landscape, and how business, society, and rules will create new ground truths for global trade.

Climate change – and our response to it – will change global supply chains in major ways. Climate change is an input to supply chains, as when a warming and more variable climate changes where crops grow, their growing seasons, and their exposure to extreme weather events. And vice versa, supply chains are an input to climate change. For example, miles traveled between an iron ore mine incurs a carbon debt in the form of transport emissions, and the energy used to transform ore into steel incurs another debt from fossil fuel combustion.

Supply chains in the age of climate change require important, and sometimes difficult, decisions about energy, geography, and physical risk. A changing global power generation mix changes the carbon intensity of production, and eventually of transportation as well. Accounting for climate in supply chains means quantifying climate impacts with a new granularity; providing that granularity will create new businesses and services. As countries seek to control their emissions and the geopolitically important supply of critical materials and products such as lithium to make batteries or advanced computing chips, new rules and regulation will become prime movers of system-level changes in what is produced, where, and how. Worldwide, companies and countries recognize decarbonization as an opportunity to shift global power structures and the most-forward-looking are planning their supply chains and resource requirements accordingly

Trade, globalization, pressure, and the present moment

The current complexity of today’s supply chains is the result of decades of growth in global trade. Trade in goods and services is not just a feature of our current economy; it has created it. Four decades ago, global merchandise exports were less than three trillion dollars (in nominal terms). By the turn of the century, and China’s accession to the World Trade Organization, that figure had doubled. It would triple before the global financial crisis, and then grow by half again by 2021, when global exports passed $22 trillion. Trade moves the global economy, but it also moves with the global economy - as evidenced by sharp drops during recessions and most recently, the Covid-19 pandemic.

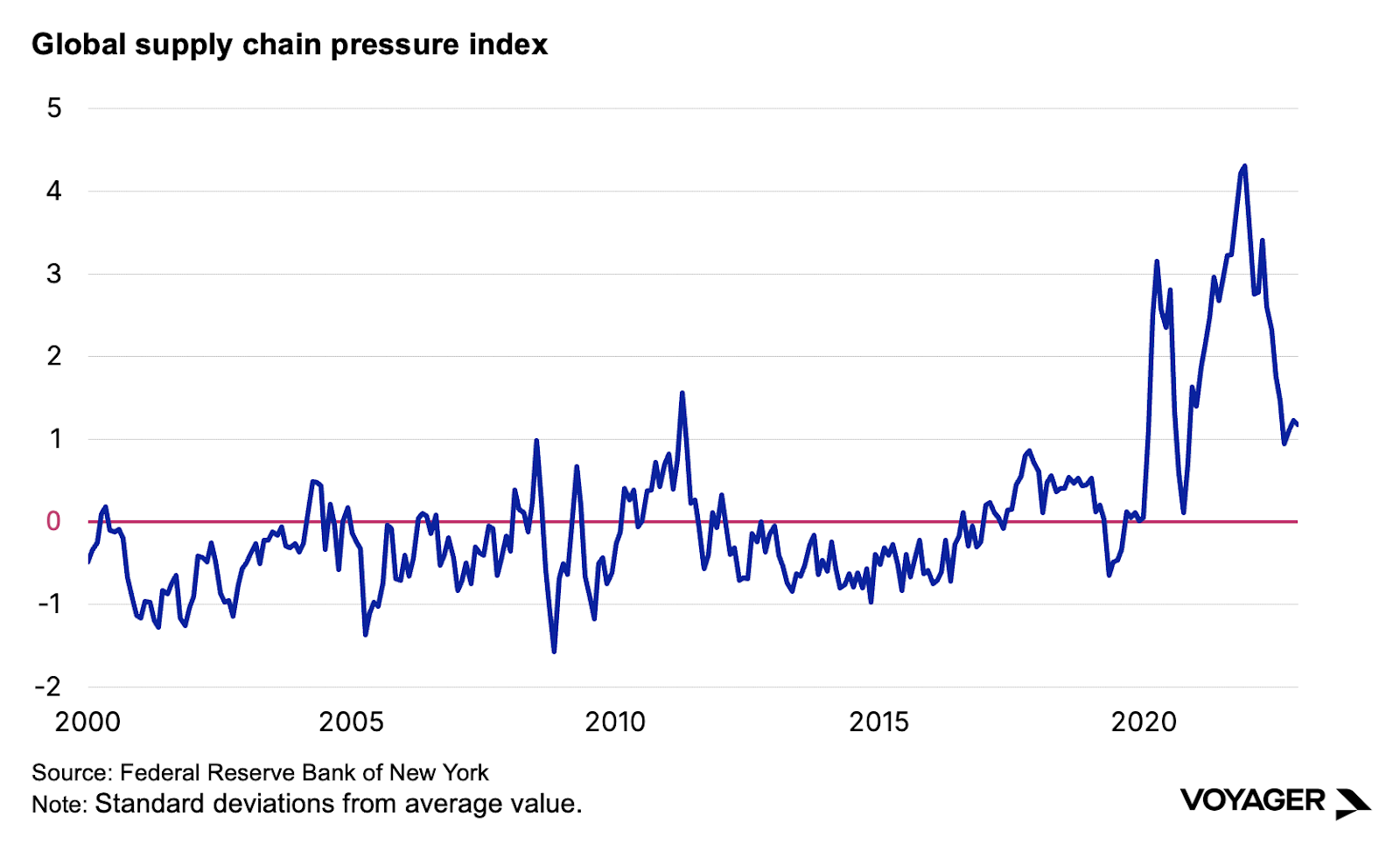

The long-term increase in global exports necessitates vast, complex supply chains working harmoniously and quickly. Break those attributes - via a global pandemic and Russia’s invasion of Ukraine for instance - and things become quite messy. Just-in-time supply chains for semiconductors break down, and simple, inexpensive chips become a major drag on automobile production. Shipping containers pile up in ports not because of lack of ships, but because of lack of berths. By the Federal Reserve Bank of New York’s measure, global supply chain pressures at the start of the pandemic were almost five standard deviations above the average. Matters have since improved, but supply chain pressure is currently higher than all but a few months of this century outside the start of Covid-19.

The corporate response to the extreme supply chain stress in that chart above is noteworthy. Three years ago, the US corporate boardroom scarcely discussed bringing production capacity back into domestic force. By the middle of last year, onshoring (establishing new domestic production), reshoring (bringing production capacity back), and nearshoring (establishing new production capacity in close geographic proximity) were mentioned nearly 200 times in a quarter. An announcement is not an ironclad commitment, but when public companies elevate these trade terms to the level of corporate disclosures and earnings calls, they are more than rhetoric.

Finally, one of the most durable modern trends in trade – growing exports from China – is showing signs of change. This will have huge ramifications for global supply chains. China’s accession to the WTO is a large part of why trade has grown so much in the past two decades, but not just as an exporter. China’s trade surplus likely hit a record in 2022, more because of weak imports than surging exports. China’s goal of creating its own domestic supply chains would further strain imports, particularly challenging major European exporters which derive substantial revenue from the country. The country is so big, and so enmeshed, in so many sectors that its unilateral moves can break global flows, as when China refused to accept plastic waste for recycling.

There is another important factor at play for global supply chains as well: China’s working population is undergoing a profound change. It is not only aging, it is also shrinking. The demographic dividend that gave us ‘workshop of the world’ of the 2000s and 2010s is now paid out. The changing workforce (not just in terms of shrinking labor supply but also the rising cost of that labor) has given some firms the impetus to move their production, at least partially. Apple, for instance, plans to move production of even some marquee products to Vietnam and India in the next few years, not just because of cost but because of the continuing effects of Covid-19 and geopolitics. JP Morgan estimates that double-digit shares of manufacturing every product except the Macbook could flow out of China in the next three years.

All of this is not to say that globalization is unwinding (in researching this letter, Voyager read more “end of globalization” essays, papers, and book reviews than it is worth counting, and most still end with a question mark). But it is nevertheless changing - and every conflict, every re-shoring, every move to Southeast Asia means that global supply chains will need new scrutiny of physical flows of goods and commodities.

New flows, new places, new imperatives

Reaching net zero global emissions in the next three decades will require extraordinary expansion of today’s supply chains critical to the energy transition, such as those for wind, solar, and hydrogen electrolyzers. It will also require the establishment and scaling of completely new supply chains. For each of these, careful measurement and reporting of key attributes (and shortcomings) will be needed to attract investment capital, withstand regulatory scrutiny, and enable producers and consumers to maximize unit economics. What is more, we must do more than just measure – we must create supply chains and systems of economic production that reduce, and eventually eliminate, negative climate system externalities. And, we must create systems that are robust to today’s physical and geopolitical disruptions, and resilient to tomorrow’s.

Some of the supply chains that will need massive expansion include:

- Energy transition minerals such as copper, nickel, and lithium

- Silicon used in photovoltaic cell manufacturing

- Rare earth metals used in electronics and permanent magnets for wind turbines

- Scaffolding materials and growth media for alternative protein production

- Green hydrogen used in industrial processes

- Synthetic fuels

- Low-carbon building materials

- Carbon dioxide processing, including direct air capture and long-term CO2 storage

Then there are new places where supply chain scrutiny will be essential:

- Resource production sites in environmentally sensitive areas

- New exporting companies where decarbonization technologies are manufactured

- Extant but under-analyzed electrical grids now powering global manufacturing

- End of life and reuse networks of lithium-ion batteries

Supply chain scrutiny will be essential where it intersects with ownership, participation, and quality of life implications for local communities. On a pure volume basis, a net-zero emissions economy will extract and consume billions of tons less material as it shifts away from combustible hydrocarbons. But, it will still require extraction of critical minerals, from thousands of sites, close by to millions of people. Extracting critical minerals cannot just be abstracted away, either. Production and material recovery techniques will improve, as will their sensitivity to the environment, but there is no escaping a step change in volume and therefore, an imperative to drive impact as close to zero as possible. Fossil fuel extraction, refining, and combustion exacts an enormous toll on the global population and the energy transition must do better.

There will also be much more than things we mine and refine going into a net zero economy. We will need better ways of producing chemicals, coatings, and materials – and we will need comprehensive, pre-emptive product lifecycle planning for everything we make. Wind turbine maker Vestas’ new roadmap for zero-waste turbines is instructive. More than 80% of its current product line can already be re-used or recycled. It now plans to end landfilling of its blades, and “view old epoxy-based blades as a source of raw material”.

Finally, there are new imperatives that supply chains must meet:

- Understanding land and water impacts from producing energy transition metals

- Articulating the precise emissions profile of each step of material production

- Ensuring that goods and services needed for decarbonization are free from human rights violations

- Tracking the emissions impacts of production delays for decarbonization technologies

Business and society will drive the initiatives outlined above. There is another, essential factor that will drive greater supply chain sophistication in the future: government action. New regulations in the EU and US will require companies to understand the climate impacts of their production cycles and balance sheets – and for many companies, to do so for the very first time.

Durable reporting obligations

In December, the European Parliament and the member states of the European Union agreed to the EU’s Carbon Border Adjustment Mechanism. The first of its kind, CBAM is meant to address the greenhouse gas emissions embedded in a number of carbon-intensive products. Initially, those are:

- Iron and steel

- Cement

- Fertilizers

- Aluminum

- Hydrogen

- Electricity

The EU also signaled intention to include plastics and chemicals by 2026, and every sector covered by the EU Emissions Trading System by the end of the decade. CBAM will begin operating in October, initially only with reporting-only obligations.

The impacts of CBAM could be quite substantial. It essentially applies carbon pricing beyond the EU’s borders to imported products. For products made with high embedded emissions, their effective cost will go up; for products with lower emissions, effective costs will be relatively lower. At a stroke, reporting on the direct and indirect emissions from producing key economic - and decarbonization - inputs will become essential for every major producer.

In the US, the Securities and Exchange Commission is finalizing a proposed rule that would require publicly-listed companies to detail their greenhouse gas emissions as well as their plans for reaching net zero emissions and their climate-related financial risks. From a supply chain perspective, the proposed rule’s significance is its requirement to report both direct and indirect emissions and its requirement that large companies provide some assurance that the information they provide is accurate. The agency has received thousands of comments during its comment period, and perhaps not surprisingly the proposed rule is something of a political football.

Like CBAM, the SEC’s rule will take time to enter effect. But the direction of travel it delineates is clear: companies will require root-level insight on their own emissions and those of their supply chains, and they will need to report them in a financially accountable and transparent manner. Adding global supply chain transparency could be as big a development for public company reporting as the initial raft of regulations passed in the wake of the great crash of 1929, that required corporate truthfulness, enabling generations of investors to put their money to work with confidence in what they were buying.

Voyager specifically avoids investing in companies, or business models, predicated purely on a short-term policy. What we see governments developing through institutions like the SEC or mechanisms like CBAM are less policies than they are rules. That is, they are becoming the new climate-related wiring, plumbing, and roads that will determine the flows of capital and goods.

In the 1930s, US regulators responded to the crisis of poor-quality market information by creating what would become the Generally Accepted Accounting Procedures (GAAP). These rules-based standards, and the principles-based IFRS standards, allow the global economy to have a shared understanding of business performance. We expect the same will emerge related to climate risk: a universal language of quantified climate risk and carbon liabilities, widespread and enduring as a global tool for corporate decision-making.

To put it another way: financial disclosure of carbon exposure is a bell that will be hard to un-ring. Borders – and global corporate strategy - once adjusted to account for carbon exposure, are unlikely to go back to what they once were.

Ground truths

Stresses and shocks are nothing new to global supply chains. Nor, for that matter, is managing them for business continuity and financial advantage. Globalization may be changing, but more than $22 trillion dollars of exports flowed between countries last year.

What is new, for global supply chains, is that they must adhere to the rules of a global economy wired for decarbonization, and the corporate (and individual) desires for clear measurement, reporting, and verification of decarbonization. Tomorrow’s supply chains need to be as low-carbon as possible, as environmentally optimized as possible, as resilient as possible, while still being as low-cost as possible. That last attribute, once paramount, can no longer be the only determining factor. Corporate net zero goals favor zero-carbon supply chains - but rules-based changes to the world’s trade and financial governance organizations will force the change.

In the effort to reach net zero emissions, supply chains will need to establish, track, and report new ground truths. That means new measurement, new verification, and new delivery of crucial information to every significant participant in global trade. It also means a big shift in comparative advantage in global business. It is no longer enough to be cheapest or fastest; it is now imperative to be cleanest, and most transparent. Some companies will adjust to carbon-conscious supply chains; some will embrace them; some will falter. And, some companies will emerge not just as participants in carbon-conscious supply chains, but as their creators.

.jpg)