.jpg)

We are proud to announce Voyager’s $275M Fund II.

With this new fund, we will continue to partner with extraordinary teams building the foundational technology companies to sustain and advance civilization. Abundance is not automatic, but it is technologically favored. We are living at the dawn of some of the most powerful technologies ever built, and their progress is compounding. Electrification, automation, artificial intelligence, and advanced manufacturing are no longer individual forces – they are converging to form the new foundations for durable growth. Alongside accelerating global demand for electricity, materials, and industrial capacity, these trends guide our investment strategy at Voyager.

FASTER EVERY DAY

In 2022, we wrote that systemic instability was accelerating – Faster Every Day. That remains true. As we also noted in Faster Every Day, so does the countervailing force: the rapid technological progress that enables societies to adapt and ultimately flourish. Over the past four years, these twin trends have intensified. Global volatility has surged, fueled by escalating geopolitical tensions, fraying trade alliances, and intensifying physical risks from climate change. Markets have adjusted accordingly. National security priorities have accelerated domestic investment in industrial capacity and critical resources. Advanced manufacturing and compute have become instruments of corporate and sovereign advantage. At the same time, demand for electricity has boomed, driven by new data centers, manufacturing, and the electrification of transportation.

In this market context, three particular technology domains continue to shape our investment strategy: energy, compute, and automation. Since we launched Voyager in 2021, advances in these three fields have compounded at an extraordinary rate. They now define the frontier of innovation and we expect their influence to grow – and accelerate – over the decade ahead.

ENERGY, COMPUTE, AND CONTROL

Now more than ever, three technological forces are rewriting the economics of cost and performance:

- Energy systems are being transformed by distributed, renewable generation, and storage.

- Computation and artificial intelligence are growing dramatically more powerful and accessible.

- AI-enabled control is extending into the physical world, optimizing machines, robotics, and systems at scale.

Individually, each trend is transformative. Together, they compound progress. As energy, compute, and production scale in tandem, physical systems become more durable and scarcity recedes. Power becomes cheaper and more reliable. Homes, factories, and infrastructure are built and maintained more efficiently. Transportation becomes safer, cleaner, and less expensive as vehicles electrify and automate. Core services improve continuously, easing strain on infrastructure and demands on finite resources. When foundations improve, the frontier of possibility also expands. Technology has made abundance more achievable than ever.

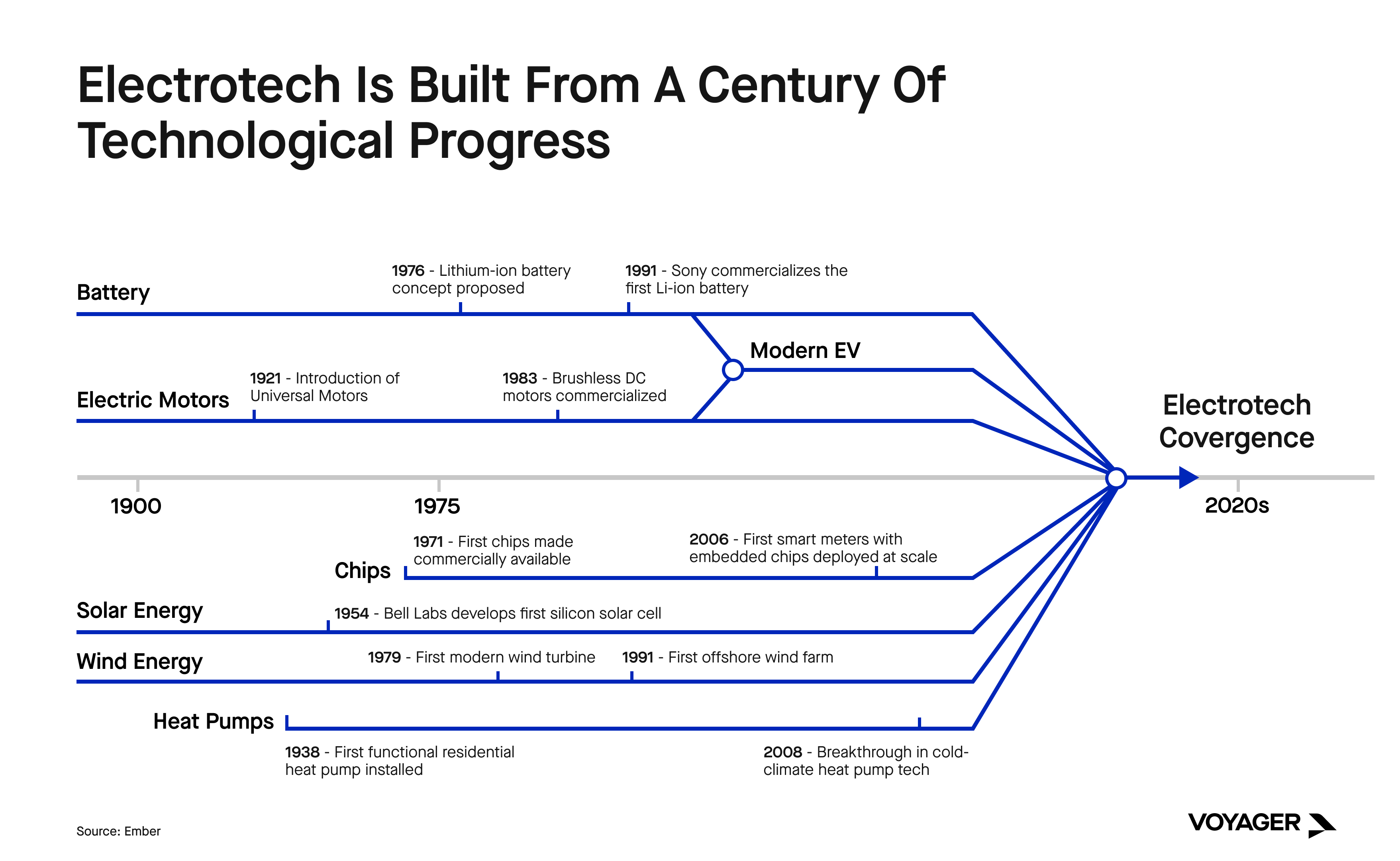

Electrification is the New Default

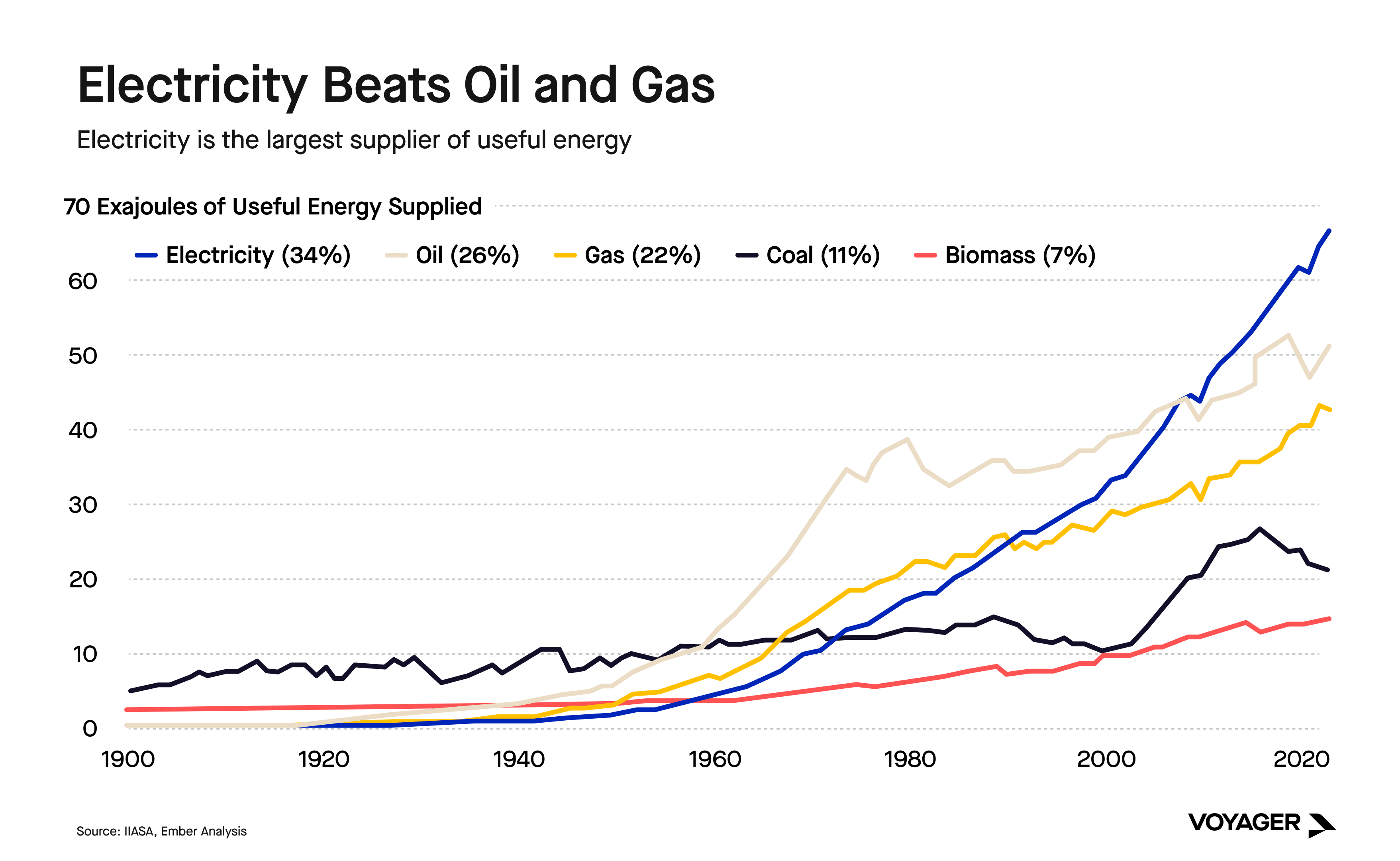

Over the past five years, electricity has become the dominant way people access energy – surpassing oil, gas, coal, and biomass. The pace of this transition is accelerating, and its largest impacts are still ahead. Technologies that have demonstrated superior economics – a category that includes technologies built on the electrotech stack of batteries, solar and electric vehicles – are winning in global markets, and will continue to win.

Cars are becoming electric by default – electric drive-trains are cheaper and better performing than internal combustion engines. Heating, cooking, and industrial processes are electrifying. Batteries, sensors, and software controls have become cheap and powerful enough not only to electrify existing machines, but to enable entirely new ones. New devices built on more powerful electrification technology range from drones and mobile robots to AI-enabled medical devices that meaningfully extend human capability.

AI’s Opportunity Surface Expands

Electrification and AI reinforce one another: as more devices become electric, more of the world becomes programmable. AI software can optimize for cost, safety, and performance across electricity grids, vehicles, factories, and fleets of machines. As the cost of powerful AI continues to decline, its opportunity surface continues to expand.

Intelligent Automation Scales

Autonomous vehicles offer a clear signal of physical AI’s march into the mainstream. In just five years, the concept of controlling machines in chaotic real-world environments has moved from experimental to commonplace. AI-driven control of physical systems is no longer a research problem – it is now a deployed and trusted capability in high-consequence daily situations.

Intelligent automation will extend far beyond transportation, controlling electric devices in our homes and offices, factories, cities, and infrastructure – and enabling new machines that were previously infeasible.

Electric and digital systems reward investment with rapid improvement, better performance, and falling costs. Fossil-based legacy systems do not: they grow more brittle and expensive over time. As finite resources dwindle, the easiest to mine deposits are depleted and costs of exploration and extraction grow. Extractive systems become harder to scale over time. In contrast, renewable technologies improve with each unit produced, benefitting from learning curves and mass manufacturing. They share many of the same components, factory equipment, and supply chains that have driven dramatic improvements in semiconductors, smartphones, and laptops.

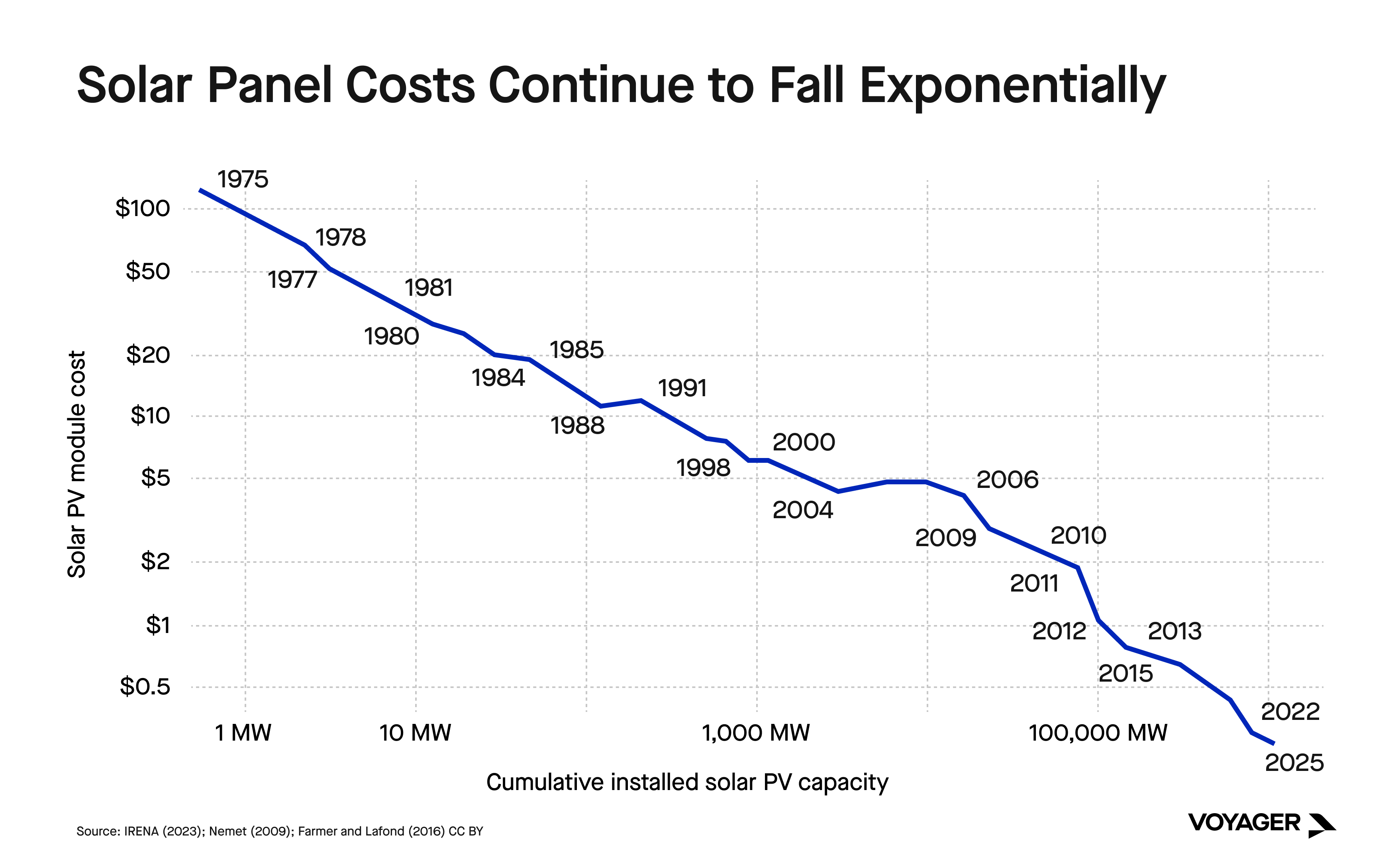

The exponential decrease in solar’s cost is accelerating its deployment – at scale. In 2024, solar accounted for 70% of new electricity generation installed around the world.

.jpg)

Each iteration of deployed electrotech fortifies the economy’s productive foundation, expanding the possibilities for what societies can achieve today and what they can build next.

THE BOTTLENECK IS PHYSICAL

In recent memory, economic expansion was dominated by ideas. The 2010s saw massive returns to growth through code. Facebook, Amazon, Apple, Netflix, and Google built platforms that centralized commerce, communication, and entertainment – scaling and reaching billions of people. The results are self-evident: in the final days of the past decade, these five companies were the most valuable in the world.

This past boom was built mainly on top of old infrastructure – installed many decades ago, on now outdated technologies, from our industrial factories to our electric grid. It worked well enough to support the trillion-dollar companies of the last cycle. Their growth did not require revisiting the fundamental systems that underpin the economy. Today, they do.

The world’s energy and manufacturing infrastructure has not kept pace with innovation. Over the past five years, shortages of chips, rare earth metals, magnets, electric motors, turbines, and grid equipment have repeatedly constrained entire industries and muted global growth. Geopolitics, war, weather events, and a pandemic exposed how brittle modern supply chains have become.

Our imagination has hit its physical limits.

The most valuable companies of this decade require a new speed and scale for energy and materials, and new systems of supply. Hyperscalers and AI companies consume massive amounts of power. Automotive companies need batteries, and the lithium that goes into them. Continued progress in AI requires the most advanced manufacturing equipment and fabs, which are produced by only a few companies. Energy systems depend on turbines, transformers, and grid capacity with multi-year lead times. In many regions, data centers are stalled not by capital or demand, but by a lack of substations and available electricity.

Fossil infrastructure compounds the problem. Beyond its inherent inflexibility and inefficiency, combustion-based generation is slow to build, expensive to maintain, and difficult to scale. Delivery backlogs for gas turbines now stretch from three to seven years, with production concentrated with a handful of suppliers. Fossil fuel prices are volatile, reflecting the fragility and geopolitical exposure of their supply chains. In contrast, renewable power is increasingly faster and cheaper to deploy, and when paired with energy storage, can outperform legacy power systems and new gas generation. Renewables have already won on the fundamentals – and they continue to improve with scale.

The constraints are tightening everywhere: energy availability, manufacturing throughput, compute capacity, and access to critical minerals. Systems once assumed to have slack no longer do: surplus grid capacity built for peak loads, just-in-time global manufacturing optimized for efficiency, and Moore’s Law delivering steady, exponential improvements in computational power. That grace is gone. To maintain their competitive advantage in a global market, countries and companies must invest in the fundamental drivers of growth. Below, we outline three opportunities to create massive, enduring value – all areas that Voyager will continue investing in.

THE NEW ARCHITECTURE OF GROWTH

One: Electrification > Combustion

Electrification is a structural upgrade to industrial systems. Legacy combustion-based systems that burn hydrocarbon fuels involve continuous extraction, transport, storage, ignition, and exhaust, losing a large share of energy along the way. In contrast, electric systems are efficient, precise, and programmable: energy can be instantaneously monitored, dispatched, and traded. Electricity delivers energy precisely down to the millivolt and microsecond and eliminates entire layers of complexity. Fewer steps mean lower cost, better reliability, and faster scaling.

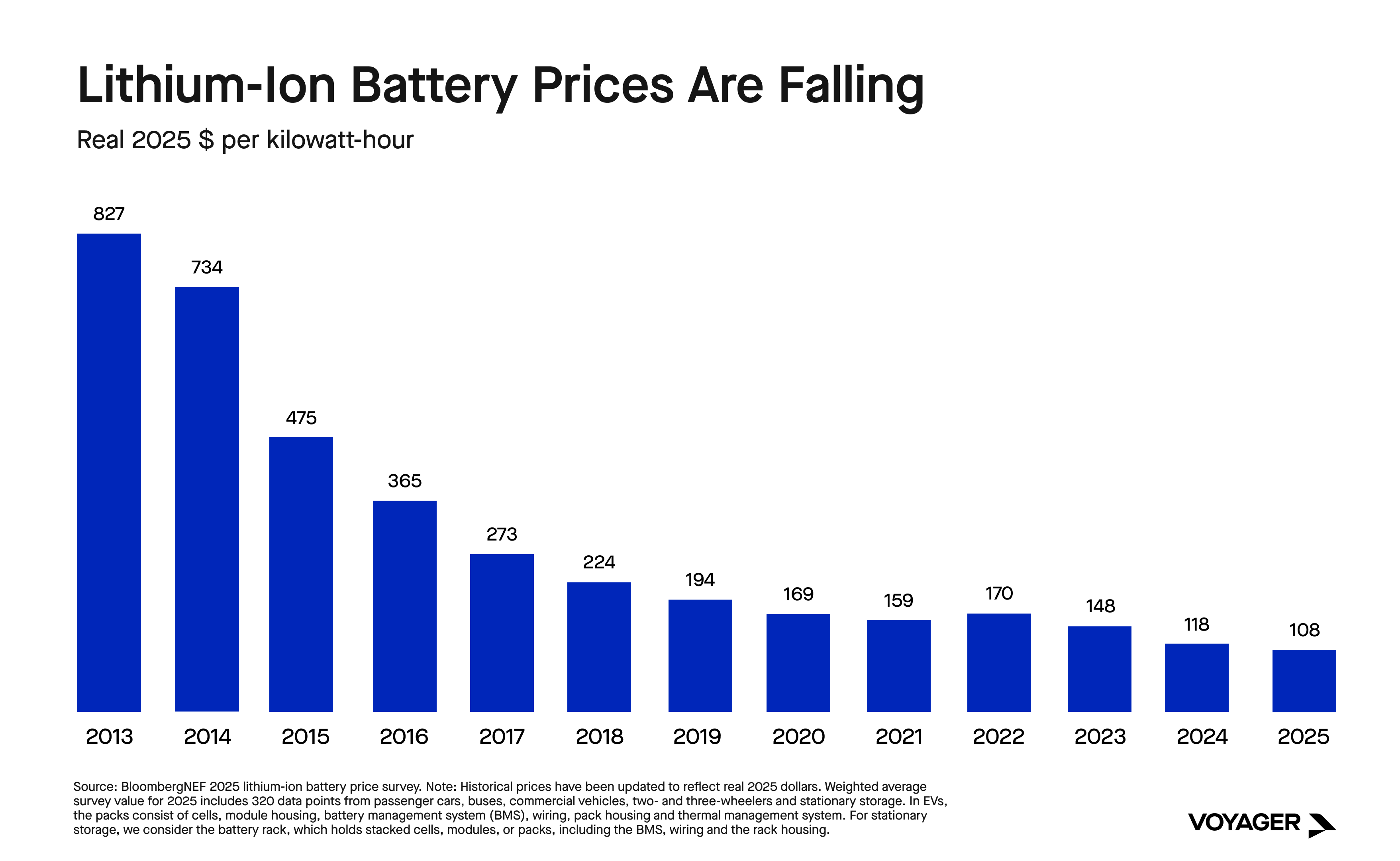

In the past five years, batteries, power electronics, and electric motors have dramatically and definitively improved. They are now cheap and powerful enough to enable more machines – and entire industries – to shift to electricity. Heat for industrial processes is moving to electric furnaces and heat pumps. Vehicles are being rebuilt around batteries and electric drivetrains as the cheapest, best option. Buildings are electrifying as electrical systems become cheaper to deliver and maintain than fossil systems. This is a whole-of-system upgrade.

Electrification also simplifies logistics. Electric heating removes the need for on-site fuel storage, constant deliveries, waste heat handling, and ventilation. Electric vehicles bypass global fuel distribution networks. Electric power routes around fuel pipes, tanks, and terminals that are increasingly constrained or stranded. In a world that must move faster, electrons are the most agile building block.

Electrification and local power generation are structural advantages. Until countries build energy supplies that are insulated from global markets, they will remain exposed to fuel price shocks. Oil and gas prices swing with conflict, cartel decisions, and demand surges. The sun does not.

Electricity is also a source of industrial leverage: the availability of electrons enables growth. Electricity determines where data centers break ground, where battery plants scale, where housing gets built. It attracts capital, concentrates talent, and converts energy into leverage. And in an economy increasingly constrained by physical resources, power unlocks everything else.

.jpg)

Two: Control of Critical Resources

For the past decades, the feedstocks of growth – fuel, compute, metals, materials – were treated as stable, global, and cheap. Supply chains were optimized for efficiency, not resilience. Companies sourced across borders. Nations assumed continuity. The result was systems that worked as long as they avoided major disruptions.

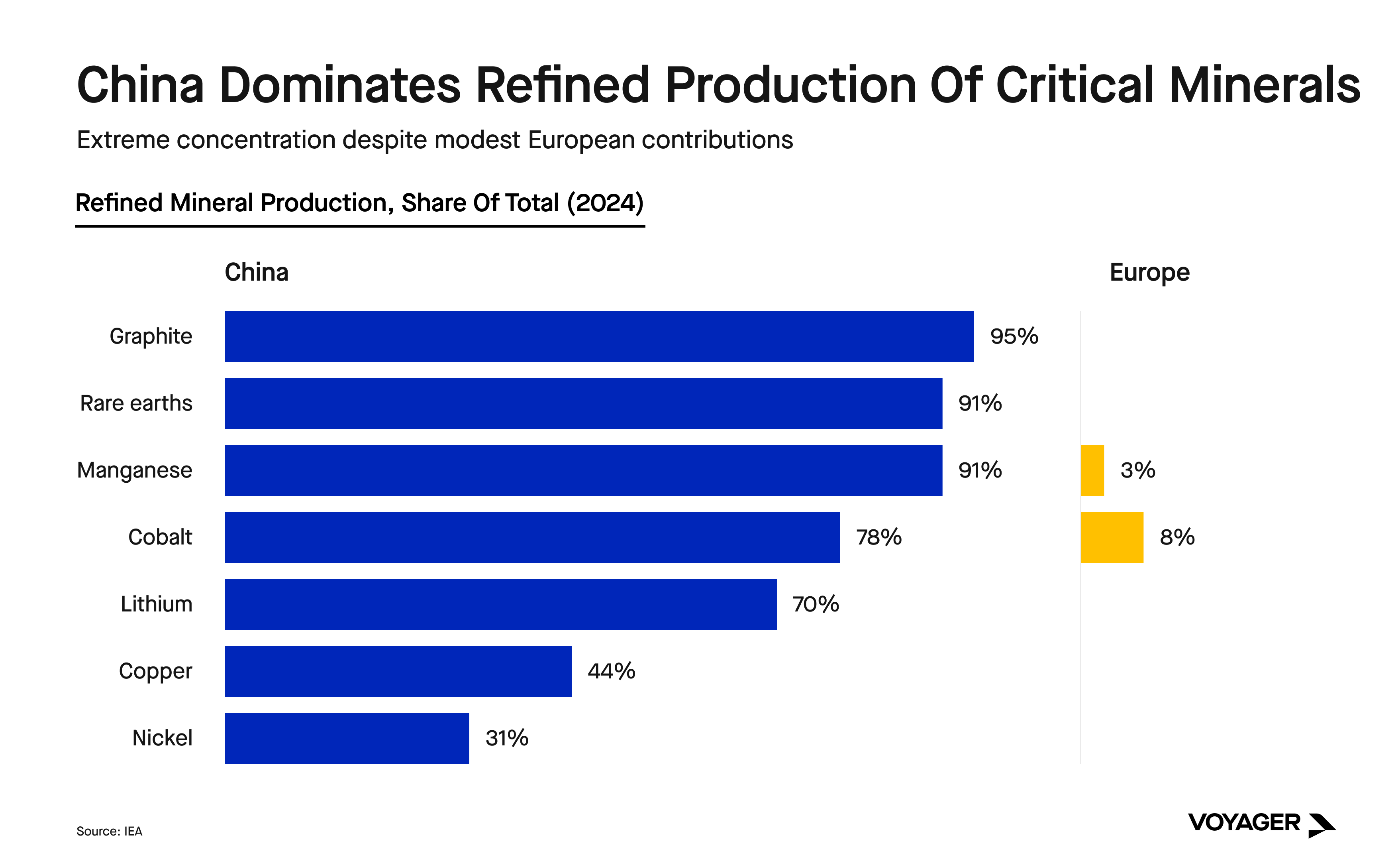

Those norms have broken. Volatility now arrives as weather, shortages, demand swings, or geopolitics – and any disruption can force the invisible hand. When Beijing recently restricted exports of rare earth metals and magnets, automakers around the globe were forced to idle their factories. When Russia invaded Ukraine in 2022, the price of gas in Western Europe skyrocketed, quadrupling home energy bills and pausing manufacturing lines. In an economy built on tightly-coupled systems, competitive advantage accrues to the companies and countries who can build and control the means of production.

Compute, energy, and materials are now strategic assets. Companies and countries are not just using computing capacity – they are building it, securing it, competing for it. Moore’s Law once delivered exponential gains on a predictable timeline: smaller transistors, better performance at lower costs, but it has hit its physical limits. Today, improving performance depends more on specialized hardware and massive physical infrastructure – compute has weight. It takes land, power, cooling, capital, and access to the advanced fabs that make the world’s most powerful chips. Like energy or steel, compute must be planned, financed, and built. Those who can reliably build and secure computing capacity now control a key resource for global growth.

Critical minerals and materials face a different set of constraints. Asymmetric advantage accrues to those with more efficient processing technologies: modular systems that require less energy, higher purity outputs, and the ability to refine local and lower-grade feedstocks. Innovation in materials processing – not extraction alone – will define the most competitive producers, and scarcity drives invention. New chemistries, substitutes, and manufacturing techniques will continue to attract investment and entrepreneurs, reducing reliance on rare, expensive, or geopolitically-concentrated resources.

This is the new logic of resource control: systematically-important commodities are instruments of competitive leverage. These are no longer simply raw materials or utility services – they are national assets, and securing these resources is a requirement for making products that can compete in the most important global markets.

Three: Advanced Manufacturing

Advanced manufacturing turns extraordinary ideas into physical reality and defines the technological frontier. Economic progress stalls when new technologies cannot be built at sufficient scale, speed, and reliability.

Production has struggled to keep pace with current demand, not to mention imagination. Lead times for transformers, turbines, high-voltage components, batteries, and advanced chips now stretch into months and years. New facilities require specialized equipment, trained labor, and grid capacity that cannot be assembled quickly.

Flexible and optimized production changes this equation. Factories informed by sensors, real-time reporting and optimization, and continuous learning systems enable production lines to adapt while running - reducing waste, boosting precision, and accelerating improvement. With AI, production shifts from being a fixed cost to a source of flexible advantage.

The real-time control possible in AI-driven manufacturing creates a new standard for precision and efficiency. AI controls also enable us to build completely new materials and machines, expanding what is possible in manufacturing. Integrated networks of AI-controlled machines can perform in ways that individual devices cannot, be they fleets of drones or EVs or thousands of machines working together in a factory.

Advanced manufacturing will continue to define the expression of human ingenuity and technological progress. Strategic leverage will continue to compound for those building and maintaining superior capacity in manufacturing – across energy, batteries, materials, vehicles, chips, and the infrastructure that supports them.

TOOLS FOR GROWTH, EVERYWHERE

Better is the only secular trend. Once a new technology clears its early adoption curve, deployment accelerates until it becomes the default. Electric drivetrains, heat pumps, solar, utility-scale batteries – these have already penetrated the market past the point of return. Cost parity cannot be reversed. Once more efficient and more reliable products have been deployed at scale, customers do not return to slower, dirtier, and more expensive technologies.

This does not mean the path is smooth. Policy distortions, interest rate swings, and geopolitical shocks continue to reshape timelines – but they will not reverse the direction of progress. Cost compression, compounding performance, and resource control are too powerful, and too closely aligned with national and corporate self-interest, to give way.

Now, more than ever, we recognize the opportunity for ambitious founders to create the technology companies that will power prosperity for decades to come. At Voyager, we are investing in people building at the edge of possibility, translating the promise of superior technology into companies that define global markets. Each company accelerates progress, expanding the aperture of technological possibility. The result is inevitably better: growth that compounds, infrastructure that holds, and a future defined by abundance.